The interest rate is the percent of principal charged by the lender for the use of its money. The principal is the amount of money lent. Banks pay you an interest rate on deposits because they borrow that money from you. Anyone can lend money and charge interest, but it's usually banks.

The Federal Reserve System is the central banking system of

the United States of America. It was created on December 23, 1913, with the

enactment of the Federal Reserve Act, after a series of financial panic led to

the desire for central control of the monetary system in order to alleviate

financial crises. The Fed's can raise, or lower interest rates based on the

current climate of the U.S Economy. Their decisions can affect the cost of

housing, cars, student loans and even the interest on your credit card — though

not all necessarily right away. And when the Fed raises rates, all sorts of

other expenses eventually tick up.

In general, movement of the Fed’s rate does not have a

large, direct impact on long-term mortgage rates. But when the Fed’s rate goes

up, banks find ways to pass their higher borrowing costs along to consumers,

and because long-term mortgage rates are set in stone, they also factor in the

anticipation of future rate increases.

The Federal Reserve

announced it would raise interest rates and steepened its outlook for

hikes in 2019 and 2020.

After a two-day meeting, the Federal Open Market Committee

unanimously voted to increase its benchmark fed funds rate by 25 basis points,

to a range of 1.50% to 1.75%. It was the sixth rate increase since late 2015,

as the US's central bank backed further away from emergency policies that

helped heal the economy after the Great Recession a decade ago.

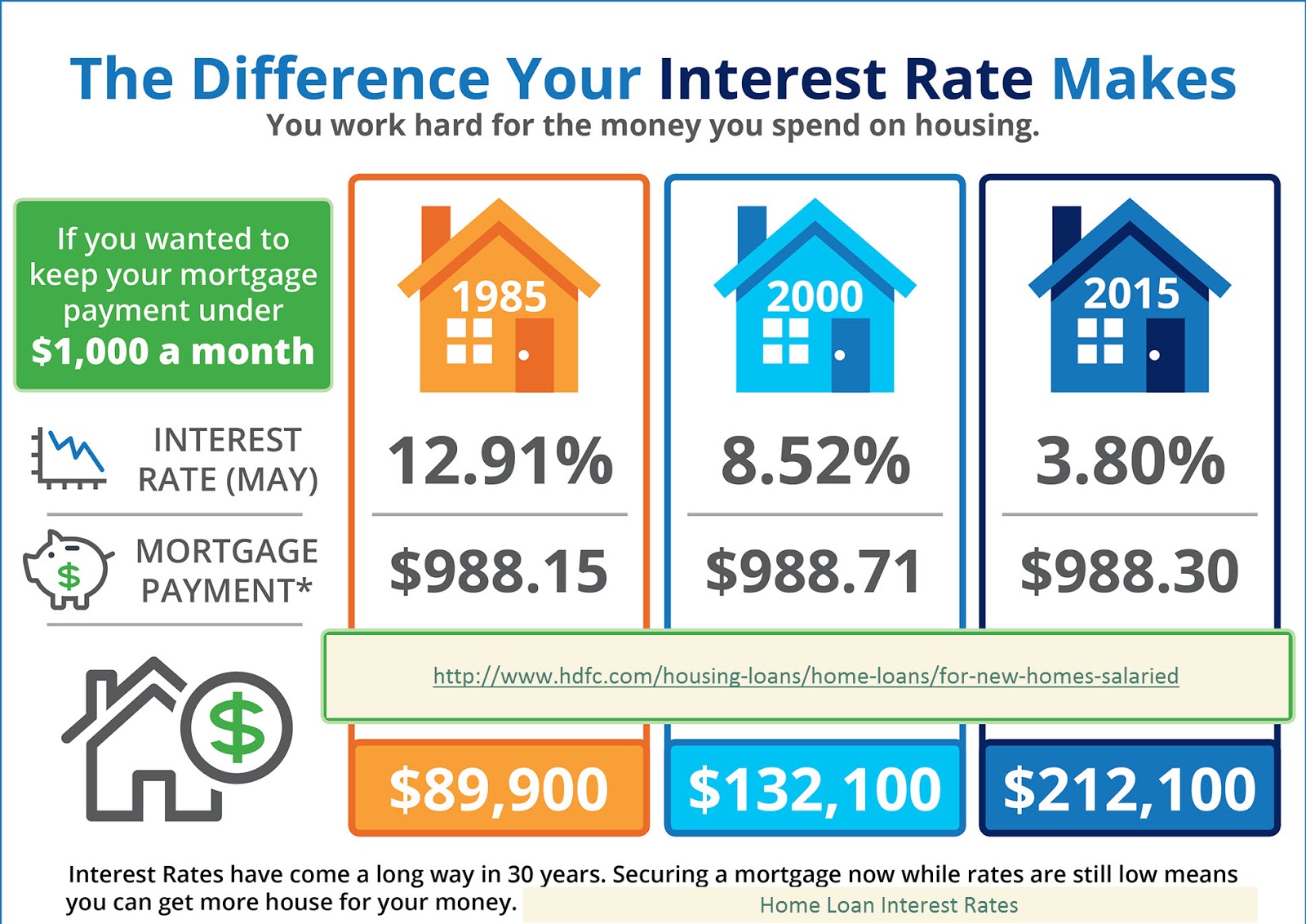

The hot economy will

continue to put upward pressure on rates. Rates are good right now as well as

our growing economy currently. This is a perfect time to get your foot in the

door on lower interest rates before they rise again. Locking in your rates

secures your payments and future in your new home. A mortgage Rate Lock is a

guarantee that the lender will deliver a specific combination of interest rate

and points if the mortgage closes by a specified date. A point is a fee or

rebate equal to 1 percent of the loan amount. Frequently, rate locks last for

30, 45 or 60 days, but they can be shorter or longer.

Many mortgage consumers wonder what the economy has to do

with mortgage rates.

Summing it up with one word: everything.

Mortgage rates tend

to be higher when the economy is doing well. That’s because inflation takes off

and investors seek higher returns than mortgage bonds can offer.

In June 2018, the unemployment rate rose to 4.0 percent. It

was 3.8 percent in May, the lowest rate since April 2000, you must go back to

the 1960s to see unemployment rates this low. There doesn’t seem to be any

cracks in the economy. Recent tax cuts have fanned the fire, and companies are

on a hiring spree.

There are several reasons to buy a home in today's market:

1.Robust Economy

2.Interest Rates are still low

3. A surge in Housing Market Inventory (more homes to choose

from)

4. Great Mortgage Packages available, even for the first-time

home buyer

One of the most listed reasons is pouring money into rent

which ends up in the pockets of someone else instead of your own. Is it time

for you to get out of someone else's home ?and into your own? If so, now is the

time to take that step, a booming economy allows buyers ease of finding their perfect

home more now than years before.

Contact Me, to see how buying a home can save you money and bring you great financial benefits too!!

Kristi Fenton

Real Estate Broker

217-617-9083-phone

217-224-8100-office

Kristibroker@gmail.com - Email

I want to extend the same friendly welcome to you also-with help purchasing or selling a home... so let's get started.